Sydney's affordability ceiling is pushing property investors toward Brisbane, Perth, and Adelaide in 2026. Gross yields in the Harbour City have compressed to around 3.1% on houses — well below the 4–5% available in competing capitals. With the RBA cash rate sitting at 4.10% following back-to-back hikes in early 2026, the numbers have become genuinely difficult to stack in Sydney for most investor profiles.

Why investors are shifting away from Sydney in 2026

For most of the last decade, Sydney was the default answer when Australian investors asked where to put their money. Deep liquidity, strong population growth, and a chronic housing undersupply made it hard to argue against. That logic has not disappeared entirely, but the conditions that made Sydney such a reliable performer have collided with a new set of headwinds that are changing the calculus for investors who are building or scaling a portfolio right now.

The median dwelling value in Sydney sat at approximately $1,292,157 as of April 2026, according to Cotality's Home Value Index, with house prices recording a quarterly decline of -1.4%. Values are now sitting roughly 1.0% below the November 2025 peak, and the top end of the market has been softening for five consecutive months. That is the headline. But for investors, the more important signal is the structural gap between what Sydney costs to hold and what it actually returns on rent.

With interest rates and property prices moving in opposite directions from investor expectations, the yield-to-borrowing-cost gap has widened to a point where Sydney property now demands a genuine long-hold thesis rather than a near-term cash flow argument.

What is driving the move out of Sydney?

Sydney's affordability and yield squeeze is a structural problem, not a cyclical blip. The gross yield on Sydney houses averages around 2.6%, while investor mortgage rates are sitting in the 6.0–6.5% range. That gap means most Sydney house investments are significantly negatively geared from day one, and with negative gearing Australia rules remaining unchanged for existing properties, carrying that shortfall becomes a real question of borrowing capacity and cash reserves.

Three forces are concentrated behind the trend:

- Entry price compression. At a median above $1.6M for houses, each 0.25% rate hike strips roughly $12,000 from average borrowing capacity. Two consecutive hikes in 2026 have removed approximately $24,000 in purchasing power per buyer — enough to move many investors into a different market altogether.

- Yield stagnation. Sydney rents rose 5.9% annually and vacancy tightened to 1.1%, which sounds positive. But when the asset base is already the most expensive in the country, rent growth of that magnitude barely moves the yield needle upward.

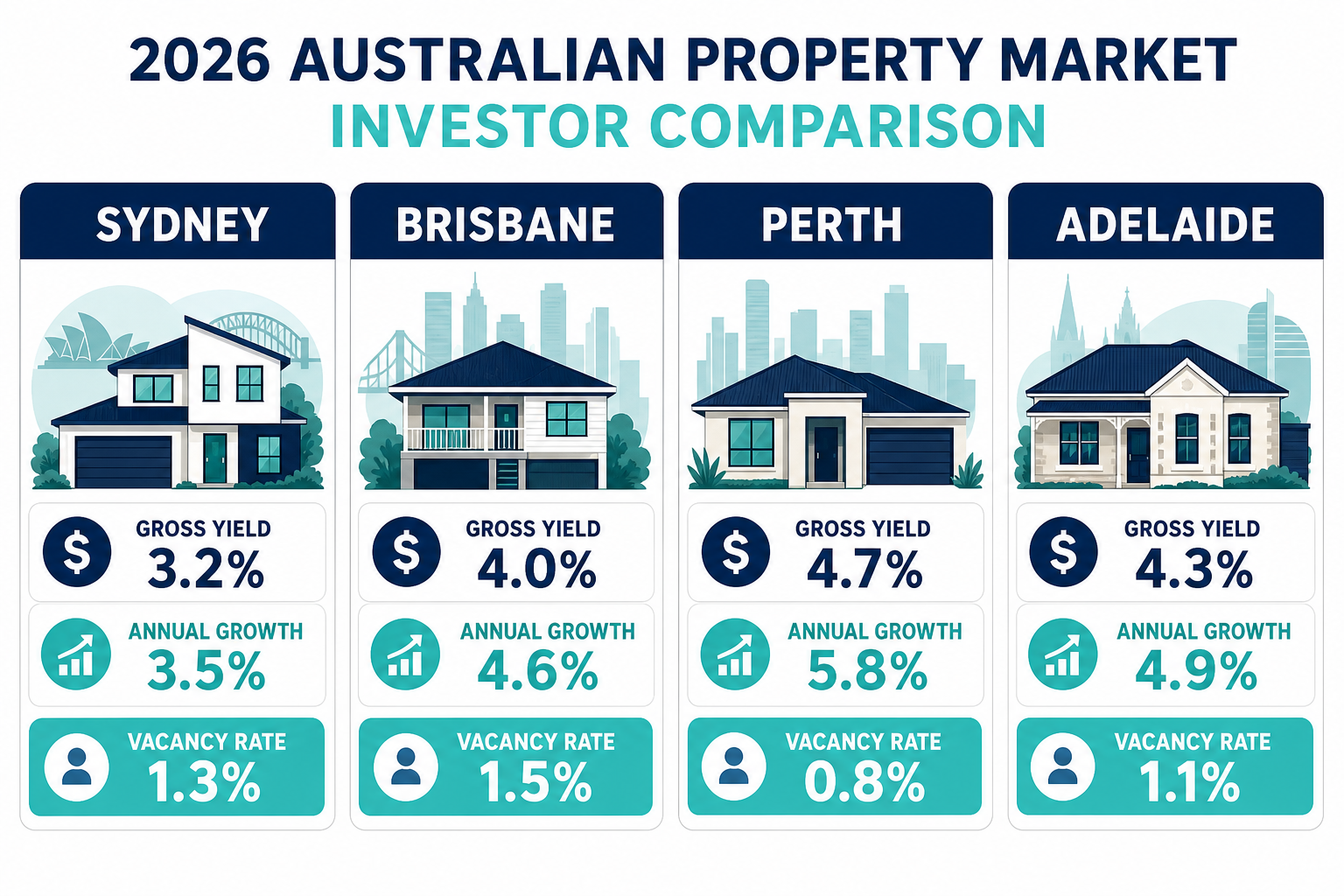

- Stronger value elsewhere. Perth recorded +24.3% annual growth, Brisbane +19.0%, and Adelaide +11.4% in the year to March 2026, according to the Cotality April 2026 data. Investors following the fundamentals are difficult to keep in a market offering marginal or declining short-term returns.

The capital growth versus cash flow debate matters here. Investors who prioritise near-term income or want a more balanced portfolio are finding that the Sydney equation increasingly requires a very long time horizon to work.

Where investors are buying instead

The redistribution of investor capital is clearly identifiable in the data. Brisbane, Perth, and Adelaide are attracting the highest share of interstate investment interest, with selected regional markets also drawing attention from yield-focused buyers.

Brisbane

Brisbane enters 2026 as Australia's strongest major-city growth story, supported by a decade-long infrastructure pipeline anchored by the 2032 Olympics and the Cross River Rail project. House price growth is forecast at 9–11% for 2026 by multiple research houses, and vacancy rates remain below 1% across most middle-ring suburbs.

Gross yields in Brisbane sit at approximately 4.5% broadly, with well-located inner-city units achieving 5.7% in submarkets like Bowen Hills and South Brisbane. The challenge is that the easy gains in blue-chip suburbs are narrowing — the median house price has crossed $1 million, and the standout value now sits in growth corridors rather than established inner-ring addresses. Investors working with Buyers Agency Australia are increasingly focused on identifying which Brisbane pockets still offer a combination of affordable entry, rental demand, and infrastructure-driven upside rather than simply buying into the city broadly.

Read More: Top Property Investment Hotspots And Strategies 2026

Perth

Perth led all Australian capitals with 24.3% annual growth to March 2026, and its vacancy rate has tightened to 0.5% — fewer than 1,000 available rentals across the entire metro. Gross yields on houses sit around 4.3%, with units delivering closer to 5.9%, according to REIWA April 2026 data.

The case for Perth is real, but some important caveats apply. The median house price is now around $845,000 — no longer a cheap entry point by historical standards. Yield compression on houses has been significant, dropping from around 5.5% two years ago to 4.3% now as prices have grown faster than rents. Single-industry exposure to the resources sector adds a risk layer that investors building across multiple markets should factor into their portfolio construction. That said, for investors targeting off-market properties in Brisbane and Perth simultaneously, the combination of tight vacancy and strong population growth from interstate migration continues to make the WA capital one of the more compelling yield-and-growth plays on the national stage.

Adelaide

Adelaide offers a different profile. Its vacancy rate of 0.8% is among the tightest in the country, and the median house price of approximately $972,000 represents a meaningful discount to Sydney and Brisbane. Five-year cumulative growth has been close to 80%, demonstrating that the market has already moved decisively — but forecasters including ANZ and KPMG still see 6–8% growth for 2026.

The key risk with Adelaide is runner length. Unlike Brisbane and Perth, which are drawing strong interstate migration flows, Adelaide's demand engine is primarily organic and local. When affordability constraints bite, the market may cool faster than others. For investors who buy carefully in supply-constrained northern and western suburbs, Adelaide remains a strong income and moderate-growth proposition.

Regional markets

Regional Queensland continues to generate some of the most compelling regional property investment numbers in the country, with markets like Townsville, Cairns, and Rockhampton regularly achieving gross yields of 6%+, driven by genuine employment demand from resources, health, and essential services. Regional WA is also delivering strong returns, with combined regional gross yields around 5.2%.

These markets carry higher risk — thinner liquidity, smaller tenant pools, and cyclical economic exposure — and require careful due diligence. They are not appropriate for every investor profile, but for those targeting positive cash flow property in Australia, selected regional markets continue to offer entry prices and yield numbers that simply do not exist in any major capital city.

Best suburbs and market types to watch

City selection alone is no longer enough to guarantee results in 2026. The "rising tide" dynamic that let investors pick almost any Brisbane or Perth suburb and expect strong returns has passed. The focus has shifted to asset selection within chosen markets.

Suburb characteristics that matter most

Investors achieving the best outcomes in 2026 are typically targeting suburbs with the following profile:

- Genuine rental demand. Low vacancy, short days-on-market for rentals, and a diversified employment base nearby. This filters out speculative markets where vacancy could spike.

- Infrastructure-driven uplift. Transport corridors, employment hubs, hospital expansions, or education anchors that are already funded and under construction — not merely announced.

- Affordability runway. Suburbs priced below the city median where borrowing capacity still allows a larger buyer pool to participate. In Brisbane, that increasingly means outer corridors and growth areas rather than inner-ring addresses.

- Supply constraint. Established suburbs with limited land release or heritage overlays that prevent oversupply from developing-grade stock.

| Market | Approx. Median (Houses) | Gross Yield (Houses) | 12-Month Growth | Vacancy Rate |

|---|---|---|---|---|

| Sydney | ~$1,600,000 | ~2.6% | ~4.4% | ~1.1% |

| Brisbane | ~$1,000,000+ | ~4.5% | ~19.0% | <1.0% |

| Perth | ~$845,000 | ~4.3% | ~24.3% | ~0.5% |

| Adelaide | ~$972,000 | ~4.8% | ~11.4% | ~0.8% |

Sources: Cotality HVI April 2026, REIWA April 2026, SQM Research April 2026

For dual income properties and co-living strategies, Brisbane and Adelaide are showing the strongest case — affordable entry prices, strong rental demand, and zoning flexibility across certain LGAs.

Sydney vs interstate: how investors are comparing the trade-offs

This is where strategy and personal circumstance diverge. Sydney is not a broken market. It has a chronic undersupply problem, 5.3 million residents, and a rental vacancy rate of 1.1% — all of which provide a structural floor under values. ANZ forecasts a modest recovery to 2.6% growth for Sydney in 2027 after a projected 0.7% fall in 2026, which suggests the city's long-term capital story remains intact.

But intact is not the same as optimal for every investor.

| Factor | Sydney | Brisbane / Perth / Adelaide |

|---|---|---|

| Entry price | $1.3M–$1.6M+ median | $845K–$1M median |

| Gross yield (houses) | ~2.6% | 4.3%–4.8% |

| Annual price growth (2025) | ~4.4% | 11%–24% |

| Vacancy rate | ~1.1% | 0.5%–1.0% |

| Rate sensitivity | High | Moderate |

| Borrowing capacity required | Very high | Moderate–high |

| Cash flow position | Deeply negative | Mildly negative to neutral |

For investors with strong existing equity and a long hold timeline, a Sydney position still makes sense — particularly in the Western Sydney infrastructure corridor where units are generating 5.8–6.6% gross yields and where population growth and government capital expenditure are concentrated. For investors working within a $700K–$1M budget, or those who need their property to carry more of its own weight from a cash flow perspective, the interstate case is considerably more compelling right now.

Understanding property investment strategy in Australia for 2026 comes down to matching market selection to individual circumstances — not following the market that is making the loudest headlines.

How Buyers Agency Australia helps investors choose the right market

Buyers Agency Australia takes a data-led approach to market selection that explicitly avoids the common mistake of chasing whatever city just posted the biggest headline number. Led by Dragan Dimovski, a property expert with 20+ years of experience across national markets, the firm combines suburb-level data analysis, AI-powered strategy planning, and genuine boots-on-the-ground presence across Sydney, Melbourne, Brisbane, Perth, and Adelaide.

The process works like this. A client's borrowing capacity, income structure, existing portfolio, risk tolerance, and investment timeline are mapped before any suburb or city is recommended. That profile is then matched against current market data — yield, vacancy rates, infrastructure pipeline, days on market, and capital growth trajectory. If a market does not pass an investment-grade threshold, it is excluded regardless of what the media is saying about it.

Many of the strongest opportunities never appear on the major listing portals. Off-market access is a significant part of what separates a well-positioned investor from one competing against the full market. Buyers Agency Australia's network consistently delivers access to properties before they reach public listing, which matters more in tight markets where the best stock disappears quickly.

If you are weighing up the Sydney versus interstate question and want to understand where your capital works hardest given your specific position, book a free strategy session with the team to map out your options.

How to decide whether to stay in Sydney or move capital elsewhere

There is no universal right answer to this question. The most useful framework considers four variables:

1. Budget and borrowing capacity

If your borrowing capacity limits you to properties priced below $900K–$1M, Sydney largely removes itself from contention for houses. The unit market in Western Sydney corridors remains accessible, but it carries different risk characteristics. Brisbane, Perth, and Adelaide all offer house-and-land options within that range, often with superior yield.

2. Investment goals: capital growth versus income

Sydney's structural undersupply case is compelling for pure capital growth over a 10-year horizon. If near-term cash flow matters — whether for serviceability, retirement income, or SMSF compliance — the interstate markets offer a far more workable income position from day one. For SMSF property investment specifically, cash flow characteristics are critical and Sydney's yield profile creates genuine compliance risk for many funds.

3. Portfolio stage and diversification

An investor with significant Sydney equity who has never owned interstate is often better positioned to deploy their next dollar elsewhere — not because Sydney will fail, but because concentration in one market adds unnecessary risk when better-yielding options are available. Diversification across two or three markets in different economic cycles is a more resilient structure.

4. Investment timeline

Sydney rewards patience more than almost any market in the country. A 15-year hold almost always looks different from a 5-year hold. If the timeline is short or uncertain, the combination of high entry price, meaningful negative gearing, and currently softening values creates a real risk of underperformance relative to capital deployed.

For most investors sitting outside Sydney with a budget under $1.2M, the data in 2026 points more clearly toward interstate than at any point in the last decade. For Sydney-based investors with existing equity and a longer runway, a selective Sydney position in infrastructure-corridor units still has merit — but it should not be the default answer by force of habit.

Key takeaways for investors planning their next purchase

The Australian property market in 2026 is operating in two distinct speeds, and the divide is structural rather than temporary. Sydney and Melbourne are managing affordability ceilings and rate sensitivity, while Perth, Brisbane, and Adelaide continue to post record values underpinned by interstate migration, tighter supply, and stronger yield fundamentals.

For investors, the practical conclusions are clear:

- Sydney's long-term capital case remains intact, but it requires a high entry price, deep negative gearing tolerance, and a long hold period to deliver.

- Brisbane, Perth, and Adelaide offer superior entry pricing, stronger yields, and near-term growth momentum — but the easy, broad-market gains in those cities are narrowing, and suburb selection now matters more than city selection.

- Regional markets in Queensland and WA continue to deliver the highest gross yields nationally, but carry liquidity and vacancy risk that requires careful management.

- The best decision is one built on individual strategy — budget, borrowing capacity, income structure, timeline, and portfolio balance — not on which city made the news this quarter.

Strategic investors who get the market selection right in 2026 are positioning themselves for the growth cycle that follows. That requires the kind of data-backed, interest-independent analysis that Buyers Agency Australia provides for clients across every major market in the country.

Ready to make a clear, evidence-based decision about where your next property should be? Book a free strategy session or contact the team to start building a property strategy tailored to your goals.

Frequently Asked Questions

Why are investors leaving Sydney in 2026?

Sydney's gross house yields have compressed to around 2.6% while borrowing costs sit near 6.5%, making cash flow difficult. Investors are finding better yield and growth combinations in Brisbane, Perth, and Adelaide.

Which city offers the best yield for property investors in 2026?

Perth leads capital cities with gross house yields around 4.3% and unit yields near 5.9%, supported by a 0.5% vacancy rate and strong resource-sector employment.

Is it still worth buying property in Sydney in 2026?

For long-hold investors with strong equity and high borrowing capacity, selected Sydney positions — particularly infrastructure-corridor units — still have merit. For budget-conscious or income-focused investors, interstate markets are more compelling.

What are the best suburbs to invest in Australia in 2026?

Brisbane growth corridors, Perth's middle-ring established suburbs, Adelaide's northern supply-constrained pockets, and regional Queensland employment hubs are among the areas showing the strongest investment fundamentals.

How does a buyer's agent help with interstate property investment?

A buyer's agent provides local market knowledge, off-market access, due diligence, and negotiation support — essential when investing outside your home state without the ability to inspect properties personally.

Leave a Reply